Global financial markets are closely monitoring a major economic transition as China’s GDP growth set to slow becomes the defining macroeconomic headline of 2026. Data compiled by international financial institutions indicates that the world’s second-largest economy is entering a period of deliberate consolidation. This shift follows a volatile sequence of geopolitical developments, persistent domestic headwinds, and realigned state priorities.

For enterprise leaders, corporate treasurers, and institutional investors, tracking this deceleration is essential for building a resilient risk-mitigation framework. As Beijing pivots away from debt-fueled expansion toward high-quality development, the ripple effects are reshaping commodity pricing, corporate supply chains, and multinational revenue targets across the globe.

Table of Contents

1. The Macro Trends: China’s GDP Growth Set to Slow Across Major Projections

The expectation that China’s GDP growth set to slow is verified by updated forecasts from major international institutions. Economic projections indicate a steady, secular deceleration as the structural drag from legacy industries counterbalances advancements in high-technology sectors.

[2024 GDP Growth: 5.0%] ───> [2025 GDP Growth: 5.0%] ───> [2026 GDP Growth Forecast: 4.4% - 4.6%]

A mid-year Reuters poll of 54 economists indicates that China’s year-on-year expansion cooled to 4.5% in the second quarter, a drop from the 5.0% pace recorded during the first quarter. This trajectory places full-year performance at the lower end of Beijing’s official growth target of 4.5% to 5.0% announced during the March legislative sessions.

The expectation that China’s GDP growth set to slow is verified by updated forecasts from major international institutions. Economic projections indicate a steady, secular deceleration as the structural drag from legacy industries counterbalances advancements in high-technology sectors. For an in-depth breakdown of global financial forecasts and comparative country data, you can view the comprehensive updates on the International Monetary Fund data portal.

To put the current slowdown into context, the table below outlines real GDP growth projections for the 2026 fiscal year from major global financial institutions:

| Institutional Forecast Provider | 2026 Real GDP Growth Projection | Core Macroeconomic Drivers Identified |

| World Bank Baseline Poll | 4.4% | Extended property sector adjustment and cautious domestic consumption. |

| International Monetary Fund | 4.4% | Structural aging demographics and lingering labor market weakness. |

| Reuters Economist Consensus | 4.6% | Export reliance amidst a global oil shock and soft retail demand. |

| Goldman Sachs Research | 4.8% | Surging AI infrastructure exports offsetting domestic property drags. |

| BBVA Research Outlook | 4.5% | Industrial supply-demand imbalances and corporate deleveraging. |

2. Structural Property Market Drags and Deleveraging Pressures

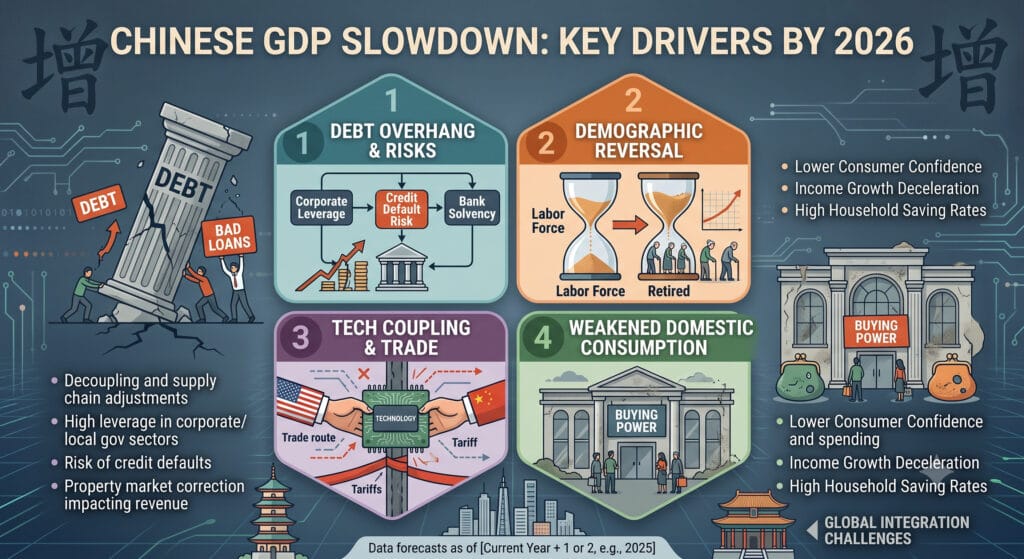

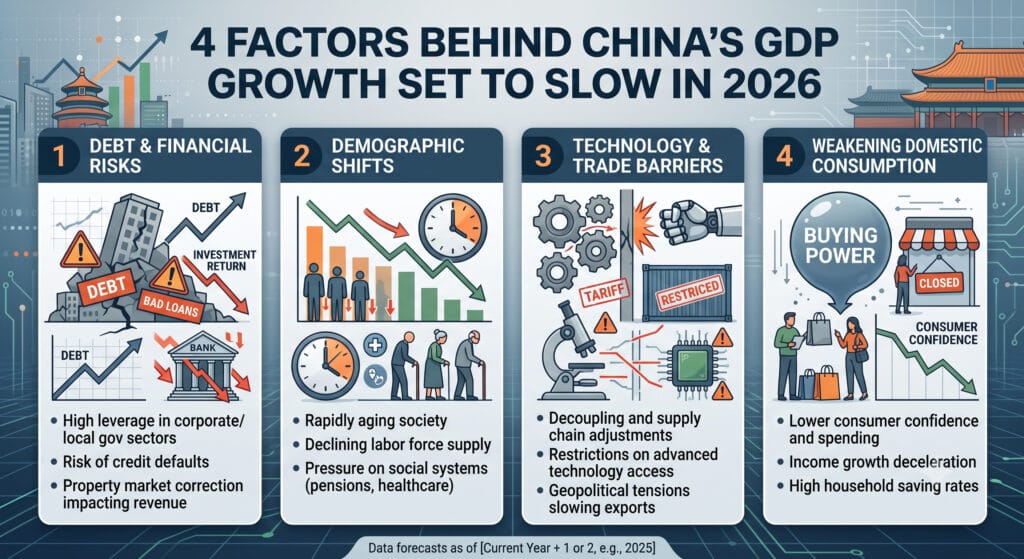

The primary structural anchor ensuring China’s GDP growth set to slow remains the ongoing correction within the domestic real estate sector. Historically accounting for nearly 25% of the nation’s total economic output, the property industry is in its fifth year of contraction. Major activity sub-indexes—including new residential housing starts, land acquisitions, and private developer investments—remain down 50% to 80% from their 2020–2021 peaks.

[Prolonged Property Downturn]

│

▼

[Depressed Household Wealth & Confidence]

│

▼

[Sluggish Domestic Consumption & Retail Sales]

│

▼

[Entrenched K-Shaped Economy & Slowing GDP Growth]

This extended property downturn impacts local government finances and household wealth. Because a large portion of Chinese household net worth is tied up in residential real estate, falling property values create a negative wealth effect that curbs consumer spending. Despite targeted public support, including credit facilities to complete pre-sold housing projects, the sector continues to pull capital away from traditional consumer-facing industries. China’s GDP Growth Set to Slow

3. The Supply-Demand Disconnect and the K-Shaped Economy

A significant internal challenge keeping China’s GDP growth set to slow is an entrenched supply-demand mismatch. Chinese industrial manufacturing shows resilience, driven by investments in advanced manufacturing, renewable energy, and artificial intelligence infrastructure. However, this supply-side strength contrasts sharply with subdued domestic consumer demand.

Macroeconomists categorize this structural divergence as an entrenched K-shaped economic trajectory:

- The Upper Arm (Strong Supply): Industrial production and green technology exports remain robust. China continues to capture global market share in electric vehicles (EVs), lithium-ion battery manufacturing, and advanced grid-management infrastructure.

- The Lower Arm (Weak Demand): Household retail sales, domestic private investment, and consumer price indexes remain soft. Wage growth trackers show deceleration, and a cautious urban labor market prompts middle-class households to increase precautionary savings rather than discretionary spending.

Because advanced tech manufacturing is capital-intensive rather than labor-intensive, strong export factories are not fully translating into a stronger consumer labor market or widespread domestic profit improvements.

According to the International Energy Agency, structural shifts in manufacturing and energy consumption are creating unique supply-demand dynamics globally. While the brief June truce allowed global oil supply to recover by 4.1 million barrels per day (bpd) to reach 98.8 million bpd, total global output sits roughly 9.4 million bpd lower than its pre-war average baseline. China’s GDP growth set to slow

4. Geopolitical Headwinds and Shifting Export Dynamics

The international trading landscape represents the final critical variable showing China’s GDP growth set to slow in the medium term. Over the past year, Chinese manufacturing firms maintained headline economic growth by expanding shipments to the Global South and accelerating deliveries to Western markets ahead of anticipated tariff modifications.

However, external demand faces headwinds from multiple directions. The combination of widening global protectionism, supply-chain localization initiatives, and volatile international energy shipping lines is raising international trade barriers. While direct U.S.-China commercial strains saw temporary stability following a leadership summit in Beijing, trade friction with mature economies remains a persistent theme. As global trade growth normalizes, China’s reliance on external export demand to offset its domestic real estate drag faces capacity constraints. China’s GDP growth set to slow

Conclusion: Strategic Fiscal Implications for Business Leaders

The consensus that China’s GDP growth set to slow does not signal an impending systemic collapse; rather, it reflects a structural transition toward a more moderate growth model. Beijing’s focus remains on high-quality development, technological self-reliance, and curbing industrial overcapacity rather than pursuing aggressive, debt-fueled GDP targets.

For global corporate strategists, this slower expansion means operating in an environment of moderate commodity demand, focused public stimulus, and highly competitive, tech-driven export pricing. Navigating this transition requires moving past outdated double-digit expansion models and focusing on the sectors driving China’s updated economic blueprint.

Frequently Asked Questions (FAQs)

Why is China’s GDP growth set to slow down in 2026?

The deceleration is primarily driven by a multi-year property market contraction, soft domestic consumer confidence, local government debt consolidation, and rising trade protectionism globally.

What are the consensus GDP growth projections for China this year?

Major institutions like the World Bank and the IMF project real GDP growth to ease to roughly 4.4% for the full year, down from the 5.0% performance recorded in prior periods.

How does the domestic property slump affect consumer spending?

Since real estate represents a primary asset for many households, falling property values reduce household net worth. This negative wealth effect prompts consumers to reduce discretionary retail purchases in favor of precautionary savings.

What sectors are showing resilience despite the broader slowdown?

China’s “new productive forces”—including electric vehicle manufacturing, solar infrastructure, lithium-ion battery technology, and AI-driven hardware exports—continue to show strong production numbers. China’s GDP growth set to slow

Disclaimer

The macroeconomic reporting and analysis provided on cfostimes.com are for general informational, educational, and corporate strategy planning purposes only. Nothing contained herein constitutes formal financial, investment, legal, or licensed commodity trading advice. Global market conditions change rapidly; readers must consult independent financial advisors before making cross-border procurement, hedging, or investment decisions based on these insights.

Dr. Dinesh Kumar Sharma is an award-winning Chief Financial Officer and Director of Finance with over 25 years of expertise in strategic planning and digital transformation. Recognized as a five-time CFO of the Year, he specializes in leveraging Generative AI and Microsoft Copilot to optimize financial forecasting and cost management. Dr. Sharma holds a Doctorate in Management (Finance) and has successfully scaled organizations from INR 1 billion to INR 7 billion. He is dedicated to providing transparent, data-driven insights for modern decision-makers at CFOs Times.