Introduction: A New Era in Indian Taxation

As of March 22, 2026, the Indian financial landscape has officially shifted. With the launch of the PRARAMBH 2026 awareness campaign by Union Finance Minister Nirmala Sitharaman, the New Income Tax Act 2025 provisions for 2026 are now the most critical focus for every taxpayer. Replacing the legacy Income Tax Act of 1961, this overhaul is not just a change in law—it is a change in the very language of finance.

The Act, which comes into effect on April 1, 2026, introduces a digital-first, trust-based framework. From the abolition of “Assessment Years” to the introduction of AI-driven assistance, this guide provides a 360-degree view of the changes every professional and student must know.

Table of Contents

1. Key Structural Changes: Moving Beyond 1961

The New Income Tax Act 2025 provisions for 2026 aim to reduce the “compliance burden” that has plagued Indian taxpayers for decades.

The End of “Previous Year” vs “Assessment Year”

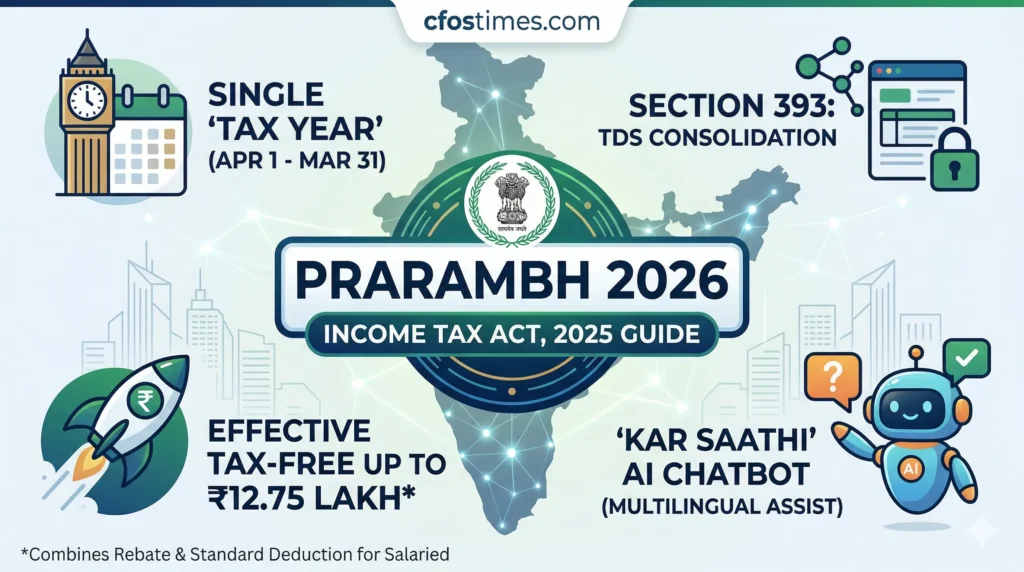

One of the most revolutionary changes is the removal of the confusing dual-year terminology. The new Act introduces a single “Tax Year” (April 1 to March 31). This alignment simplifies reporting and ensures that the year in which you earn is the same year for which you are evaluated.

Section 393: TDS Consolidation

Under the old regime, TDS provisions were scattered and complex. The 2025 Act consolidates these under Section 393. This makes it significantly easier for deductors to comply and for taxpayers to track their credits through the new Income Tax Website 2.0.

2. Tax Rates and Slabs for FY 2026-27 (Tax Year 2026)

The New Tax Regime is now the default option. To encourage adoption, the government has widened the slabs, providing significant relief to the middle class.

Detailed Tax Slab Table (New Regime)

| Income Slab (₹) | Tax Rate | Notes |

| 0 – 4,00,000 | Nil | Basic Exemption Limit |

| 4,00,001 – 8,00,000 | 5% | – |

| 8,00,001 – 12,00,000 | 10% | Fully Covered by Rebate (if total < 12L) |

| 12,00,001 – 16,00,000 | 15% | – |

| 16,00,001 – 20,00,000 | 20% | – |

| 20,00,001 – 24,00,000 | 25% | – |

| Above 24,00,000 | 30% | Highest Tax Bracket |

3. Major Taxpayer Benefits: The ₹12.75 Lakh “Zero-Tax” Milestone

One of the most trending topics under the New Income Tax Act 2025 provisions for 2026 is the effective tax-free limit for salaried individuals.

- Enhanced Section 87A Rebate: The rebate has been increased to ₹60,000. This effectively means that anyone earning up to ₹12,00,000 pays zero tax.

- Standard Deduction Increase: Salaried employees now enjoy a flat deduction of ₹75,000.

- The Math: By combining the ₹12 Lakh rebate limit and the ₹75,000 standard deduction, a salaried individual with an income of ₹12,75,000 can effectively pay zero tax under the new regime.

4. Digital Transformation: Kar Saathi and Website 2.0-New Income Tax Act 2025 provisions for 2026

The Press Information Bureau (PIB) recently highlighted the launch of “Kar Saathi.” This AI-enabled chatbot is designed to handle queries regarding the New Act, Rules, and Forms in real-time.

Why Kar Saathi is a Game Changer: New Income Tax Act 2025 provisions for 2026

- Multilingual Support: Available in 10 regional languages.

- Instant Clarification: Reduces the need for expensive tax consultants for basic filing queries.

- Accuracy: Directly linked to the CBDT’s latest circulars, ensuring 100% compliant advice.

5. Compliance and Procedural Updates

The New Income Tax Act 2025 provisions for 2026 provide a much-needed “safety net” for honest taxpayers who make errors.

- ITR-U (Updated Returns): Taxpayers now have 48 months (4 years) from the end of the tax year to correct their returns.

- TDS on Rent: The threshold for TDS on rent has been raised; it now applies only if the annual rent exceeds ₹6,00,000.

- Self-Occupied Property: You can now declare up to two houses as self-occupied with a ‘Nil’ annual value, a major benefit for those owning homes in two different cities.

Frequently Asked Questions (FAQs)-New Income Tax Act 2025 provisions for 2026

What is the PRARAMBH 2026 campaign?

It is a nationwide multimedia initiative launched on March 20, 2026, to educate the public on the transition from the 1961 Act to the New Income Tax Act 2025.

Is the Old Tax Regime still available?

Yes, the Old Regime continues to exist. However, you must actively opt for it during filing. It remains beneficial for those with high home loan interest (Section 24) or large 80C/80D investments.

What are Virtual Digital Assets (VDAs) in the new Act?

The Act formally defines VDAs to include cryptocurrencies and tokenized assets, mandating stricter reporting but providing a clearer legal framework for digital investors.

How does the ₹12.75 Lakh tax-free limit work?

It is a combination of the ₹12 Lakh income limit (covered by the ₹60,000 rebate under Section 87A) plus the ₹75,000 Standard Deduction.

Conclusion: Empathy and Technology in Tax

The New Income Tax Act 2025 provisions for 2026 represent a shift toward “Nagrik Devo Bhava” (Citizen is God). As Hon. Finance Minister Sitharaman noted, the goal is to shift behavior from “avoidance to trust.” For the finance community at cfostimes.com, this is the time to lead the conversation, helping peers and clients navigate a simpler, more stable tax future.

Disclaimer:

The information provided in this article, including the analysis of the New Income Tax Act 2025 Provisions for 2026 campaign, is for educational and informational purposes only. While we strive to provide 100% accurate and up-to-date financial data as of March 22, 2026, tax laws are subject to frequent amendments and official government notifications.

The content on cfostimes.com does not constitute professional tax, legal, or investment advice. Every individual’s financial situation is unique; therefore, we strongly recommend consulting with a Certified Chartered Accountant (CA) or a qualified tax professional before making any decisions based on this guide. cfostimes.com is not responsible for any financial loss or legal discrepancies arising from the use of this information. For official guidance, always refer to the Income Tax Department of India and official PIB releases.

Dr. Dinesh Kumar Sharma is an award-winning Chief Financial Officer and Director of Finance with over 25 years of expertise in strategic planning and digital transformation. Recognized as a five-time CFO of the Year, he specializes in leveraging Generative AI and Microsoft Copilot to optimize financial forecasting and cost management. Dr. Sharma holds a Doctorate in Management (Finance) and has successfully scaled organizations from INR 1 billion to INR 7 billion. He is dedicated to providing transparent, data-driven insights for modern decision-makers at CFOs Times.