Small and medium-sized enterprises (SMEs) across the United Kingdom face a persistent challenge when expanding globally: securing low-value working capital loans. While larger conglomerates easily navigate high-value credit lines, thousands of ambitious smaller businesses frequently hit roadblocks when applying for cross-border financing.

To bridge this specific financing gap, Chancellor of the Exchequer Rachel Reeves officially announced the UKEF British Business Bank joint scheme 2026 on July 12, 2026. Set for a full operational launch in Spring 2027, this strategic public partnership combines the unique underwriting capabilities of UK Export Finance (UKEF) with the established commercial lender distribution network of the British Business Bank.

By pooling sovereign risk mitigation tools, this joint venture aims to unlock millions of pounds in scalable credit facilities—such as term loans and flexible working capital—for underserved businesses across all economic sectors.

Table of Contents

The Strategic Architecture of the Joint Public Finance Partnership

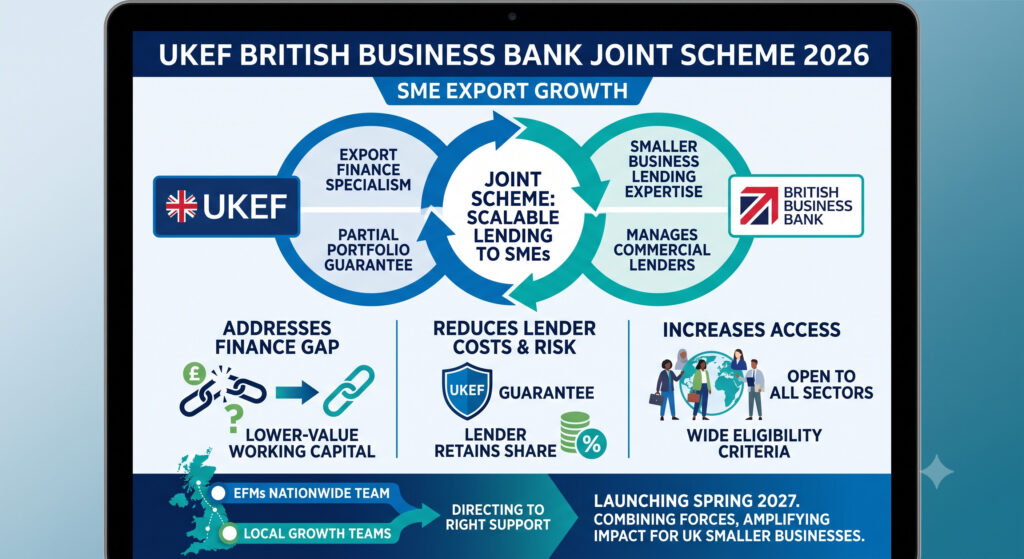

The primary structural goal of the UKEF British Business Bank joint scheme 2026 is to lower the capital allocation hurdles and underwriting costs that prevent commercial high-street banks from extending export credit to smaller firms.

Historically, assessing small-scale cross-border trade transactions carried prohibitive risk-to-reward ratios for private lenders. The newly designed model remedies this market failure through a coordinated division of institutional responsibilities:

- Risk Underwriting (UKEF): As the UK’s official export credit agency, UKEF will provide a state-backed portfolio guarantee covering a significant portion of eligible, aggregate losses within a lender’s small-business export portfolio.

- Lender Management (British Business Bank): Leveraging its extensive history of running national programs, the British Business Bank will handle the frontline execution—onboarding, assessing, and managing the participating commercial financial institutions.

Private lenders do not offload all liabilities; instead, they retain a residual share of the operational credit risk. This retention ensures strict compliance and high underwriting standards while expanding their risk appetite to serve previously unviable borrowers. UKEF British Business Bank joint scheme 2026

How the Portfolio Guarantee Risk-Sharing Framework Operates

Unlike traditional trade facilities that require individual, case-by-case transaction approvals, the UKEF British Business Bank joint scheme 2026 operates on an aggregated portfolio-level loss guarantee framework. This structural design allows commercial lenders to automatically include qualified small-business loans within the government-backed umbrella, accelerating processing times from weeks to days.

The operational flow between public agencies, commercial financial institutions, and the exporting small business follows a clear, four-stage integration pathway:

1.Origination of Small-Scale Commercial Trade Facilities:Phase 1: Facility Structuring.

Commercial financial institutions originate export-focused term loans or flexible working capital facilities for qualified SME clients who possess clear international trade ambitions.

2.Portfolio Aggregation and Loss-Share Underwriting:Phase 2: Risk De-risking.

The individual facilities are pooled into an eligible SME trade portfolio. UKEF applies its sovereign guarantee to a defined portion of portfolio-level losses, while the primary bank retains a calculated slice of risk to align institutional incentives.

3.Cross-Agency Compliance Verification:Phase 3: Operational Support.

UKEF’s nationwide team of Export Finance Managers coordinates with the British Business Bank’s Local Growth Team, verifying regional alignment and providing targeted digital support to underserved communities.

4.Capital Distribution and Export Fulfillment:Phase 4: Liquidity Deployment.

The de-risked trade credit is released to the exporting business, allowing the firm to confidently fulfill international purchase orders, fund cross-border procurement, and expand its global market footprint. UKEF British Business Bank joint scheme 2026

Key Performance Indicators: Growth Guarantee Expansion vs. Export Scheme

The launch of the UKEF British Business Bank joint scheme 2026 coincides with a wider, structural overhaul of UK small-business support initiatives announced by the Treasury. To maximize macroeconomic impact, the government simultaneously expanded the core Growth Guarantee Scheme (GGS), creating a multi-layered financial safety net for domestic and international corporate operations.

The table below contrasts the operational parameters of the existing Growth Guarantee Scheme with the newly announced joint export initiative:

| Operational Metric | The Growth Guarantee Scheme (GGS Expansion) | UKEF British Business Bank Joint Scheme 2026 |

| Primary Economic Objective | Domestic asset investment, local business scaling, and regional job creation. | Unlocking lower-value working capital and term loans for cross-border trade. |

| Underwriting Structure | Direct 70% government guarantee on individualized commercial debt facilities. | Aggregate, portfolio-level loss-sharing guarantee with risk retention. |

| Maximum Company Turnover | Elevated from £45 million to £54 million to accommodate larger scale-ups. | Open broadly to all qualified small and medium-sized enterprises across sectors. |

| Maximum Loan Term Length | Extended up to 10 years for facilities valued up to £1.1 million. | Tailored to fit standard trade transaction cycles and short-to-mid term working capital windows. |

| Projected Lending Impact | Engineered to unlock an extra £6.5 billion in market lending over four years. | Expected to channel hundreds of millions of pounds into underserved exporters. |

Macroeconomic Impact on Global Competitiveness and Trade Deals

The launch of the UKEF British Business Bank joint scheme 2026 arrives at a crucial turning point for British international trade policy. To review current legislative mandates, businesses can reference the full Small Business Strategy Reports on Parliament.uk to understand the evolving regulatory landscape confronting domestic enterprises.

According to the government’s official news brief on the UKEF and British Business Bank Joint Release via GOV.UK, the department provided over £11 billion in loans, insurance policies, and guarantees over the previous fiscal year, protecting up to 85,000 domestic jobs.

However, historically, a large percentage of that capital favored multi-million-pound engineering, defense, and infrastructure contracts.

By building wide eligibility criteria directly into this joint initiative, the British Business Bank and UKEF ensure that micro-exporters can seamlessly leverage new international trade corridors. This approach democratizes access to capital, allowing small businesses to expand their reach far beyond traditional domestic boundaries.

Step-by-Step Corporate Strategy to Leverage the Scheme

For small-business owners, corporate treasurers, and financial controllers aiming to maximize their borrowing capacity under the new framework, proactive balance sheet preparation is essential. UKEF British Business Bank joint scheme 2026

[Target SME Exporter]

├── 1. Financial Audit (Optimize Debt-to-Equity & AR Turnover)

├── 2. Pipeline Mapping (Document International Purchase Orders)

└── 3. Institutional Outreach (Engage Regional EFM & BBB Accredited Lenders)

- Optimize Working Capital Ratios: Before commercial lenders onboard portfolios into the scheme, they will assess standard credit metrics. Clean up outstanding domestic accounts receivable and maintain a healthy debt-to-equity ratio.

- Document Your Export Pipeline: Ensure all international purchase orders, letters of intent, and cross-border supply contracts are thoroughly documented. Lenders look for clear repayment pathways linked to global sales.

- Engage Local Growth Networks: Do not wait until Spring 2027 to build connections. Reach out to a regional UKEF Export Finance Manager alongside the British Business Bank’s Local Growth Team to identify accredited commercial lenders early.

Conclusion: Driving the Future of Small-Business Exporting

The UKEF British Business Bank joint scheme 2026 represents a timely alignment of structural risk-sharing and targeted economic support. By establishing an aggregate portfolio-level loss guarantee framework, the initiative successfully removes the traditional barriers that kept high-street banks from funding smaller trade deals.

As the program moves toward its formal deployment in Spring 2027, it stands to transform UK international competitiveness, giving smaller enterprises the liquidity required to turn local innovations into profitable global ventures.

FAQs: UKEF British Business Bank Joint Scheme 2026

To satisfy search intent, clear up commercial lending confusion, and secure maximum domain optimization, these frequently asked questions target the precise technical parameters of the newly announced partnership.

1. What exactly is the UKEF British Business Bank joint scheme 2026?

The UKEF British Business Bank joint scheme 2026 is a state-backed public finance initiative announced on July 12, 2026. It is structured specifically to assist small and medium-sized enterprises (SMEs) with international trade ambitions that traditionally struggle to secure credit.

The partnership bridges this funding gap by combining the sovereign export credit underwriting capabilities of UK Export Finance (UKEF) with the wholesale commercial lender onboarding and management infrastructure of the British Business Bank.

2. How does the portfolio-level loss guarantee work under this scheme?

Unlike historical trade finance facilities that required manual, transaction-by-transaction assessments by government underwriters, this scheme utilizes an aggregate portfolio-level model.

UKEF provides a pre-approved sovereign guarantee covering a fixed percentage of eligible losses across a bank’s entire small-business export lending pool. Commercial banks retain a residual portion of the operational credit risk to maintain standard due diligence. This approach minimizes lender costs and enables rapid, scalable deployment of debt capital.

3. When will the UKEF British Business Bank joint scheme 2026 become operational?

While the strategic partnership was officially unveiled in July 2026 by Chancellor Rachel Reeves, the formal operational rollout and lender onboarding framework are scheduled to launch in Spring 2027.

During the current transitional phase, private financial institutions are adjusting their underwriting criteria to align with the scheme’s wide eligibility baselines.

4. What types of financial debt facilities are covered under the framework?

The joint initiative is open to SMEs across all economic sectors and is engineered to support short-to-medium-term credit requirements. The primary lending facilities available through accredited commercial banks will include:

- Flexible Working Capital Loans: To fund upfront international procurement, manage cash flow gaps, and cover supply chain overheads.

- Structured Term Loans: To finance capital investments required to scale operations for major foreign purchase orders.

5. How does this export initiative differ from the expanded Growth Guarantee Scheme (GGS)?

While both programs are managed by the British Business Bank to unlock access to commercial credit, they serve distinct strategic purposes:

- The Growth Guarantee Scheme (GGS) focuses primarily on domestic expansion, asset acquisition, and local scaling by providing a 70% government guarantee on individual facilities up to £2 million.

- The UKEF British Business Bank joint scheme 2026 specifically targets cross-border trade constraints by offering a streamlined portfolio-level loss-sharing mechanism focused heavily on lower-value export working capital.

6. How can an eligible SME prepare to apply before the Spring 2027 launch?

SMEs should proactively prepare their financial profiles to satisfy participating commercial lenders:

[SME Pre-Application Check]

├── Balance Sheet Audit (Verify Debt-to-Equity & Current Ratios)

├── Trade Verification (Document Verified International POs / Contracts)

└── Network Engagement (Connect with Regional EFMs & BBB Teams)

First, optimize short-term liquidity ratios and clear up domestic accounts receivable metrics. Second, build a clear audit trail of foreign customer demand, including international purchase orders or letters of intent.

Finally, connect with a regional UKEF Export Finance Manager (EFM) alongside the British Business Bank’s Local Growth Team to identify which commercial lenders are fast-tracking their onboarding processes. Highly Authoritative FAQs: UKEF British Business Bank Joint Scheme 2026

To satisfy search intent, clear up commercial lending confusion, and secure maximum domain optimization, these frequently asked questions target the precise technical parameters of the newly announced partnership.

1. What exactly is the UKEF British Business Bank joint scheme 2026?

The UKEF British Business Bank joint scheme 2026 is a state-backed public finance initiative announced on July 12, 2026. It is structured specifically to assist small and medium-sized enterprises (SMEs) with international trade ambitions that traditionally struggle to secure credit.

The partnership bridges this funding gap by combining the sovereign export credit underwriting capabilities of UK Export Finance (UKEF) with the wholesale commercial lender onboarding and management infrastructure of the British Business Bank.

2. How does the portfolio-level loss guarantee work under this scheme?

Unlike historical trade finance facilities that required manual, transaction-by-transaction assessments by government underwriters, this scheme utilizes an aggregate portfolio-level model.

UKEF provides a pre-approved sovereign guarantee covering a fixed percentage of eligible losses across a bank’s entire small-business export lending pool. Commercial banks retain a residual portion of the operational credit risk to maintain standard due diligence. This approach minimizes lender costs and enables rapid, scalable deployment of debt capital.

3. When will the UKEF British Business Bank joint scheme 2026 become operational?

While the strategic partnership was officially unveiled in July 2026 by Chancellor Rachel Reeves, the formal operational rollout and lender onboarding framework are scheduled to launch in Spring 2027.

During the current transitional phase, private financial institutions are adjusting their underwriting criteria to align with the scheme’s wide eligibility baselines. UKEF British Business Bank joint scheme 2026

4. What types of financial debt facilities are covered under the framework?

The joint initiative is open to SMEs across all economic sectors and is engineered to support short-to-medium-term credit requirements. The primary lending facilities available through accredited commercial banks will include:

- Flexible Working Capital Loans: To fund upfront international procurement, manage cash flow gaps, and cover supply chain overheads.

- Structured Term Loans: To finance capital investments required to scale operations for major foreign purchase orders.

5. How does this export initiative differ from the expanded Growth Guarantee Scheme (GGS)?

While both programs are managed by the British Business Bank to unlock access to commercial credit, they serve distinct strategic purposes:

- The Growth Guarantee Scheme (GGS) focuses primarily on domestic expansion, asset acquisition, and local scaling by providing a 70% government guarantee on individual facilities up to £2 million.

- The UKEF British Business Bank joint scheme 2026 specifically targets cross-border trade constraints by offering a streamlined portfolio-level loss-sharing mechanism focused heavily on lower-value export working capital.

6. How can an eligible SME prepare to apply before the Spring 2027 launch?

SMEs should proactively prepare their financial profiles to satisfy participating commercial lenders:

[SME Pre-Application Check]

├── Balance Sheet Audit (Verify Debt-to-Equity & Current Ratios)

├── Trade Verification (Document Verified International POs / Contracts)

└── Network Engagement (Connect with Regional EFMs & BBB Teams)

First, optimize short-term liquidity ratios and clear up domestic accounts receivable metrics. Second, build a clear audit trail of foreign customer demand, including international purchase orders or letters of intent. UKEF British Business Bank joint scheme 2026

Finally, connect with a regional UKEF Export Finance Manager (EFM) alongside the British Business Bank’s Local Growth Team to identify which commercial lenders are fast-tracking their onboarding processes. UKEF British Business Bank joint scheme 2026

Financial Disclosure & Editorial Disclaimer:

The analysis presented about UKEF British Business Bank joint scheme 2026 on CFOs Times (cfostimes.com) is compiled exclusively for informational, educational, and macroeconomic tracking purposes. None of the structural breakdowns, corporate strategic steps, or financial insights provided within this article constitute formal investment, legal, or institutional credit advice. Business owners, corporate treasurers, and financial controllers must consult certified financial advisors, legal counsel, or accredited lenders before entering into cross-border credit frameworks or formal portfolio guarantee agreements. While all data points accurately reflect official public policy announcements as of July 12, 2026, operational guidelines are subject to revision by UK Export Finance and the British Business Bank prior to the Spring 2027 programmatic rollout.

Dr. Dinesh Kumar Sharma is an award-winning Chief Financial Officer and Director of Finance with over 25 years of expertise in strategic planning and digital transformation. Recognized as a five-time CFO of the Year, he specializes in leveraging Generative AI and Microsoft Copilot to optimize financial forecasting and cost management. Dr. Sharma holds a Doctorate in Management (Finance) and has successfully scaled organizations from INR 1 billion to INR 7 billion. He is dedicated to providing transparent, data-driven insights for modern decision-makers at CFOs Times.