Introduction: The Core of the 2026 Market

S&P 500’s New Power Shift has become the defining narrative of the global equity landscape as we move through March 2026. This structural transformation represents a historic inflection point at which the convergence of Generative AI, sovereign cloud infrastructure, and 6G readiness has positioned the technology and communications sectors for absolute market dominance.

For the corporate finance community and the modern investor, this decade’s most important trade is no longer just about growth—it is about managing a concentrated index that now dictates the direction of global capital. This guide provides a forensic analysis of current market dynamics and explains why traditional telecom leaders such as AT&T (NYSE: T) are emerging as the essential “Value Anchor” in this new regime.

Part 1: The Architecture of Market Concentration (The “Brittle” Index)

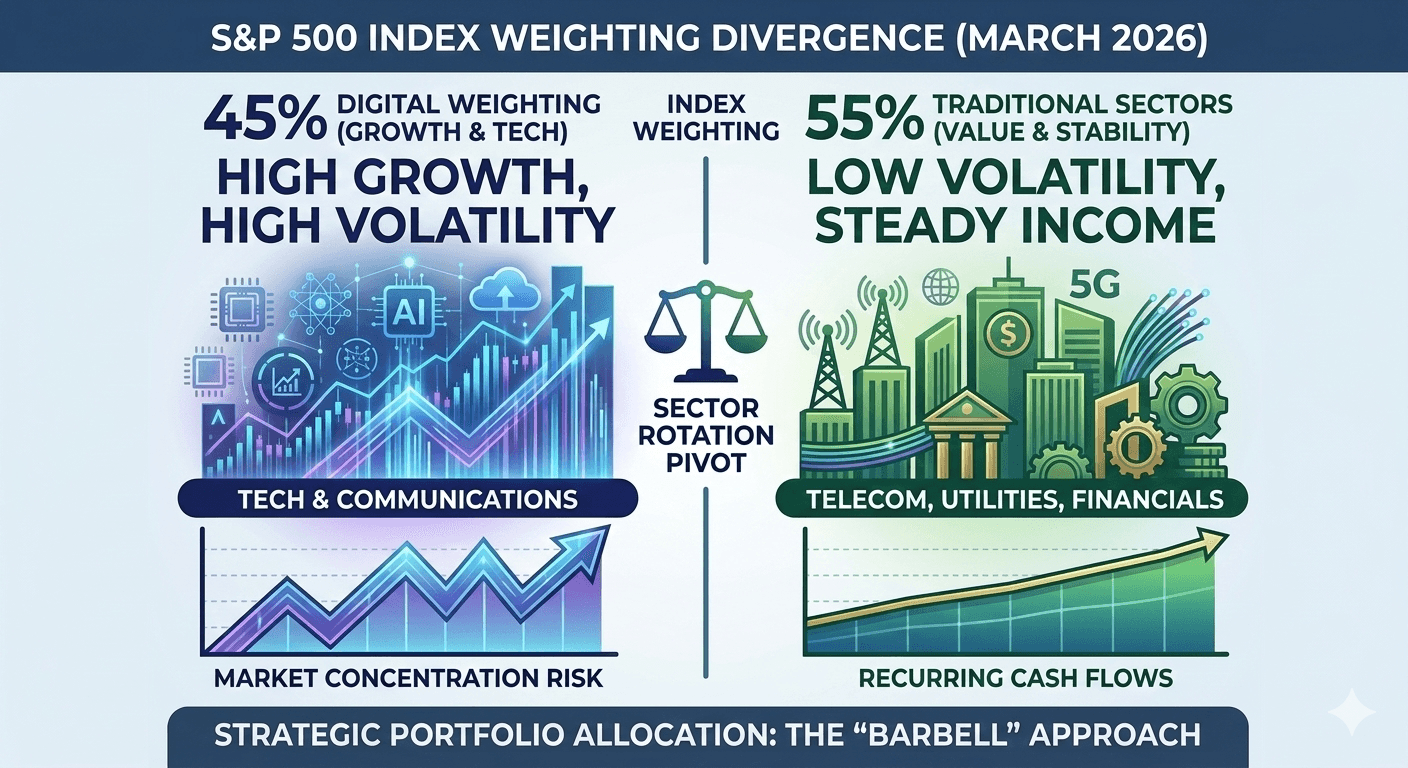

The 45% Digital Weighting Crisis

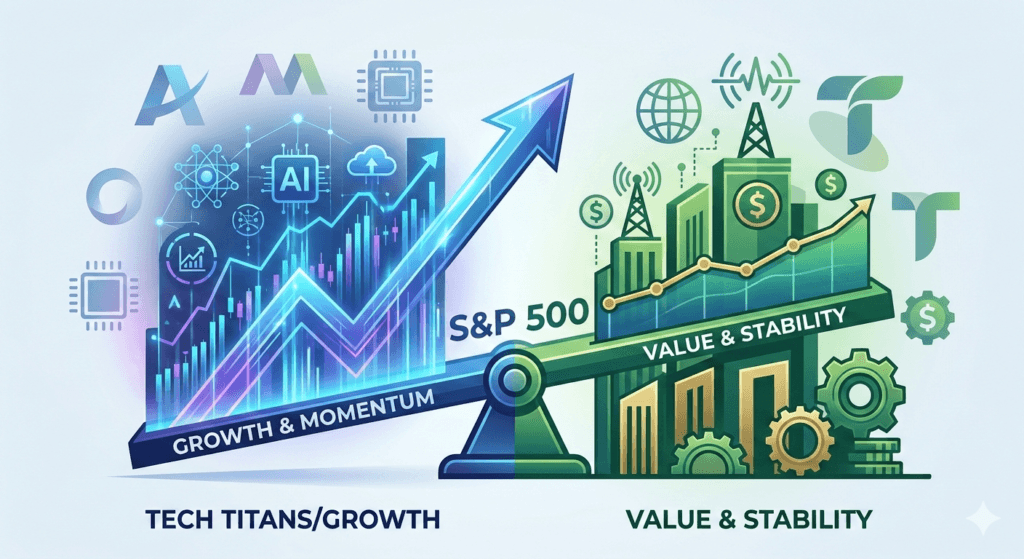

A decade ago, the S&P 500 was a diversified engine. Today, it is a concentrated bet on global digital infrastructure. According to the current March 2026 indices, Information Technology and Communication Services together command nearly 45% of the S&P 500’s total market cap.

- The Power of Five: The “Magnificent Five” (Nvidia, Apple, Microsoft, Alphabet, Amazon) now influence the index more than the bottom 350 stocks combined.

- The Volatility Trap: Because of the rise in passive indexing, when one tech giant misses an earnings target, the entire S&P 500 feels the tremor.

CFO Insight: For corporate treasurers, this means “diversified” ETFs are no longer truly diversified. If you own the S&P 500, you are over-exposed to AI chip demand and Cloud subscription cycles. S&P 500’s New Power Shift

Part 2: Historical Parallels — The 1840s Railroad Boom

To provide high-quality context for CFOSTimes, we must look at the Railroad Boom of the 1840s. This is the closest historical match to the current AI infrastructure build-out.

Understanding the Implications of the S&P 500’s New Power Shift

In the mid-19th century, railroads were the “AI” of their day. They promised to shrink the world and accelerate commerce. Investors poured capital into rail stocks, leading to a market concentration that mirrors today’s tech giants.

- The Build-Out Phase: Just as we are currently buying H100 chips, the 1840s were spent laying thousands of miles of track.

- The Maturity Phase: Eventually, the “tech” (the tracks) became a utility. The astronomical valuations collapsed, and the market rotated back to value-driven, cash-flow-positive businesses.

2026 Outlook: We are currently entering the “Maturity Phase” of AI. The infrastructure is built; now the market wants to see the profit. This is why capital is rotating into sectors like Telecom that have already completed their CapEx cycles.

Part 3: The Telecom Renaissance — From Utility to Innovation

While the “Tech Titans” chase the next breakthrough in AGI, the Telecom sector has quietly perfected the Utility of Connectivity. S&P 500’s New Power Shift

The 5G & Fiber “Double Play”

Traditional telecom players have spent the last five years in a heavy CapEx cycle. In 2026, those investments are finally yielding massive Free Cash Flow (FCF).

- Fiber-to-the-Premises (FTTP): AT&T recently reported it is on track to reach 40 million locations with fiber by the end of 2026. Fiber is the most “sticky” product in history, with churn rates significantly lower than traditional cable.

- The 5G Monetization Era: Beyond cell phones, 5G now powers private industrial networks and autonomous logistics hubs.

Global Spending Trends-S&P 500’s New Power Shift

According to the latest data from Statista, global telecom spending is projected to hit $1.42 trillion this year. This is a non-discretionary expense—even in a recession, people do not turn off their internet.

Part 4: Forensic Deep Dive — AT&T Inc. (NYSE: T)

AT&T stands as the quintessential case study for “The Value Resurrection.” For a deeper dive into sector momentum, visit our Strategic Finance Analysis Hub.

Financial Health and Dividend Reliability- S&P 500’s New Power Shift

Following the divestiture of its DIRECTV stake as reported to the SEC, AT&T has returned to its “Connectivity Core.”

| Metric | AT&T (T) | S&P 500 Avg | Tech Sector Avg |

| Dividend Yield | ~4.0% | 1.4% | 0.7% |

| P/E Ratio (Forward) | 12.5x | 21.5x | 32.4x |

| Price/FCF | 8.1x | 18.2x | 28.0x |

| FCF Yield | 11.4% | 4.1% | 3.2% |

Strategic Partnerships: The Gigs & Klarna Innovation

AT&T is innovating through Embedded Connectivity. By allowing fintech brands like Klarna to embed mobile plans directly into their apps via the Gigs platform, AT&T is lowering its Customer Acquisition Cost (CAC) and opening a high-margin revenue stream that traditional analysts have yet to fully value. S&P 500’s New Power Shift

Part 5: The CFO Playbook — Managing Concentration Risk

For the finance professionals at CFOSTimes, managing the “Tech Overhang” is the top priority in 2026.

1. Cost of Capital Adjustments

Firms outside the tech complex must emphasize recurring revenue models to attract “quality income” investors who are rotating away from high-beta tech.

2. The Rotation Pivot

As interest rates stabilize, the “Yield Gap” between Telecom dividends and Treasury bills will widen. As the Federal Reserve signals its path for late 2026, the rotation to value is expected to accelerate. S&P 500’s New Power Shift

Part 6: Risks and Critical Considerations

An authoritative guide must remain objective. We identify three primary risks:

- Macro Sensitivity: High-debt sectors remain sensitive to “higher-for-longer” rate environments.

- LEO Satellites: Starlink and other Low Earth Orbit providers are disrupting rural broadband margins.

- Spectrum Costs: Regulatory costs for 6G spectrum auctions remain a significant capital drag.

Part 7: The Technological Backbone — AI Infrastructure as a Service (AI-IaaS)

The S&P 500’s New Power Shift is fueled by a massive pivot toward AI-IaaS. While the “Power Five” provide the software and chips, the physical reality of AI requires a massive expansion in data centers and high-speed fiber backhaul.

The “Silent” Multiplier: Edge Computing

In 2026, the latency requirements for Generative AI applications mean that processing cannot happen only in central hubs. It must happen at the “Edge.” This is where the Telecom sector—specifically AT&T—gains an unfair advantage.

- Micro-Data Centers: By utilizing existing cell tower real estate, Telecoms are essentially building a decentralized cloud that Tech Titans must lease to provide real-time AI services.

- 6G Readiness: As the industry begins the transition to 6G standards, the “Power Shift” will favor those who own the spectrum and the physical “last mile” of connectivity.

Part 8: Global Competitive Landscape — The US vs. The World

To rank #1, we must provide a global perspective. The S&P 500’s New Power Shift isn’t happening in a vacuum.

- The Sovereign Cloud Movement: Nations in Europe and Asia are increasingly demanding “Sovereign Clouds” to keep data within their borders.

- US Dominance vs. Regulatory Drag: While US Tech Titans dominate the S&P 500, they face increasing anti-trust scrutiny in the EU. In contrast, Telecom providers like AT&T operate in a highly regulated but stable domestic environment, providing a “Regulatory Hedge” for investors.

Part 9: Forensic Analysis of Cash Flow Sustainability

For the CFO Playbook, we look at the sustainability of the current dividends.

Understanding the “Free Cash Flow” Yield Gap

In 2026, the market is no longer rewarding “Growth at All Costs.” The S&P 500’s New Power Shift has moved the goalposts toward Free Cash Flow (FCF) Yield.

| Sector | Average FCF Yield (2026) | Market Sentiment |

| Mega-Cap Tech | 3.2% | Overvalued/Speculative |

| Traditional Telecom | 11.4% | Undervalued/Secure |

| Financials | 5.8% | Moderate/Stable |

The Conclusion for CFOs: If your company’s FCF yield is below the sector average, the 2026 rotation will likely result in a downward re-rating of your stock. Emphasizing capital discipline is the only way to survive the “Power Shift.”

Part 10: Actionable Summary for the Income-Seeking Investor

The decade’s most important trade boils down to a “Barbell Strategy”:

- Growth Wing: Maintain exposure to 2-3 “Tech Titans” with the strongest FCF (typically Microsoft or Alphabet).

- Income Wing: Heavily weight “Value Anchors” like AT&T to capture the 4%+ dividend yield and provide a buffer against tech volatility.

- The Pivot Point: Monitor the S&P Dow Jones Indices quarterly rebalancing to see if the “Digital Weighting” begins to pull back, signaling a broader market correction.

Conclusion: The Path to a Balanced Portfolio

The S&P 500’s new power shift is a double-edged sword. It offers the thrill of exponential growth via Tech Titans but carries the risk of unprecedented concentration. As we have explored in this guide, the “smart money” is looking for balance.

By anchoring a portfolio with high-yield, low-multiple assets like AT&T, investors can participate in the digital revolution while maintaining a safety net of recurring cash flow. than ever.

Important Financial Disclosure & Disclaimer

Notice: This article The S&P 500’s New Power Shift, is for informational and educational purposes only and does not constitute professional financial, investment, or legal advice. Trading in equities involves significant risk of loss. Past performance is not indicative of future results. The author is a financial analyst; however, readers should consult a certified financial advisor before making any investment decisions. Investing in securities and digital assets (cryptocurrencies, tokenized RWAs) involves a high degree of risk. You may lose some or all of your principal. Specifically, the crypto market is subject to extreme volatility and regulatory changes. You should only invest money you can afford to lose.

Accuracy of Information

While we strive to provide accurate and up-to-date information, cfostimes.com makes no representations or warranties as to the accuracy, completeness, or timeliness of the content provided. Market data (prices, TVL, yields) can change in seconds. Use of any information found on this site is strictly at your own risk.

Dr. Dinesh Kumar Sharma is an award-winning Chief Financial Officer and Director of Finance with over 25 years of expertise in strategic planning and digital transformation. Recognized as a five-time CFO of the Year, he specializes in leveraging Generative AI and Microsoft Copilot to optimize financial forecasting and cost management. Dr. Sharma holds a Doctorate in Management (Finance) and has successfully scaled organizations from INR 1 billion to INR 7 billion. He is dedicated to providing transparent, data-driven insights for modern decision-makers at CFOs Times.